The Debt Trap – ‘Chakravyuh’

The Debt Trap – ‘Chakravyuh’

On the auspicious occasion of Diwali when everyone preaches goddess Lakshmi to bring prosperity and wealth, many are struggling to get their long-stuck homes across the country and have been hit on a crossing from all 4 sides,

- Monthly EMI burdenon their under-construction homes,

- Monthly Rent paymentsresulting in dual burden of EMI & Rent,

- Salary cuts/job loss/income loss, and

- Significant Health riskcaused by the pandemic

More than 2,00,000 stalled units in Top 7 cities of the country in approx. 250+ projects, launched either in 2013 or before, due to liquidity issue or litigation. 66% of these units are already sold. NCR market holds 60% of these under construction units spread over 67 projects with 70% units already sold. In Mumbai Metropolitan Region nearly 38,060 units stalled across the city. However, the number of projects covering stuck units in this region is spread over 89 projects as against 67 projects in NCR. (Source: Anarock research)

Also, the Indian Real Estate developer’s debt burden has more-than-trebled over the last decade to approx. INR 4,00,000 crs in 2018 from INR 120,000 crs in 2009. In terms of units, volumes of sales have gone up 1.28 times while inventory has increased 3.33 times between 2009 and 2018. In the past 10 years, while the value of sold stock increased 1.56 times, the value of unsold stock has increased 4.72 times. (Source: Economic Times 5 Feb,2019). This sector is struggling since 2017 post Demonetization, RERA approval lags, increase in transaction cost to 19% (12% GST + 7% stamp duty) on under construction units, money diversion from projects for expansion/servicing debt obligations of other projects and finally the collapse of shadow banking/HFC’s after IL&FS burst, the only major source of funding of Real Estate projects.

Thus, while debt has grown in a monumental manner but so has inventory. Sales did not go up in the same proportion. Having borrowed money from different sources, developers kept adding housing stock into the market without productivity. And then came COVID 19 that derailed it completely further impacting the buying capacity.

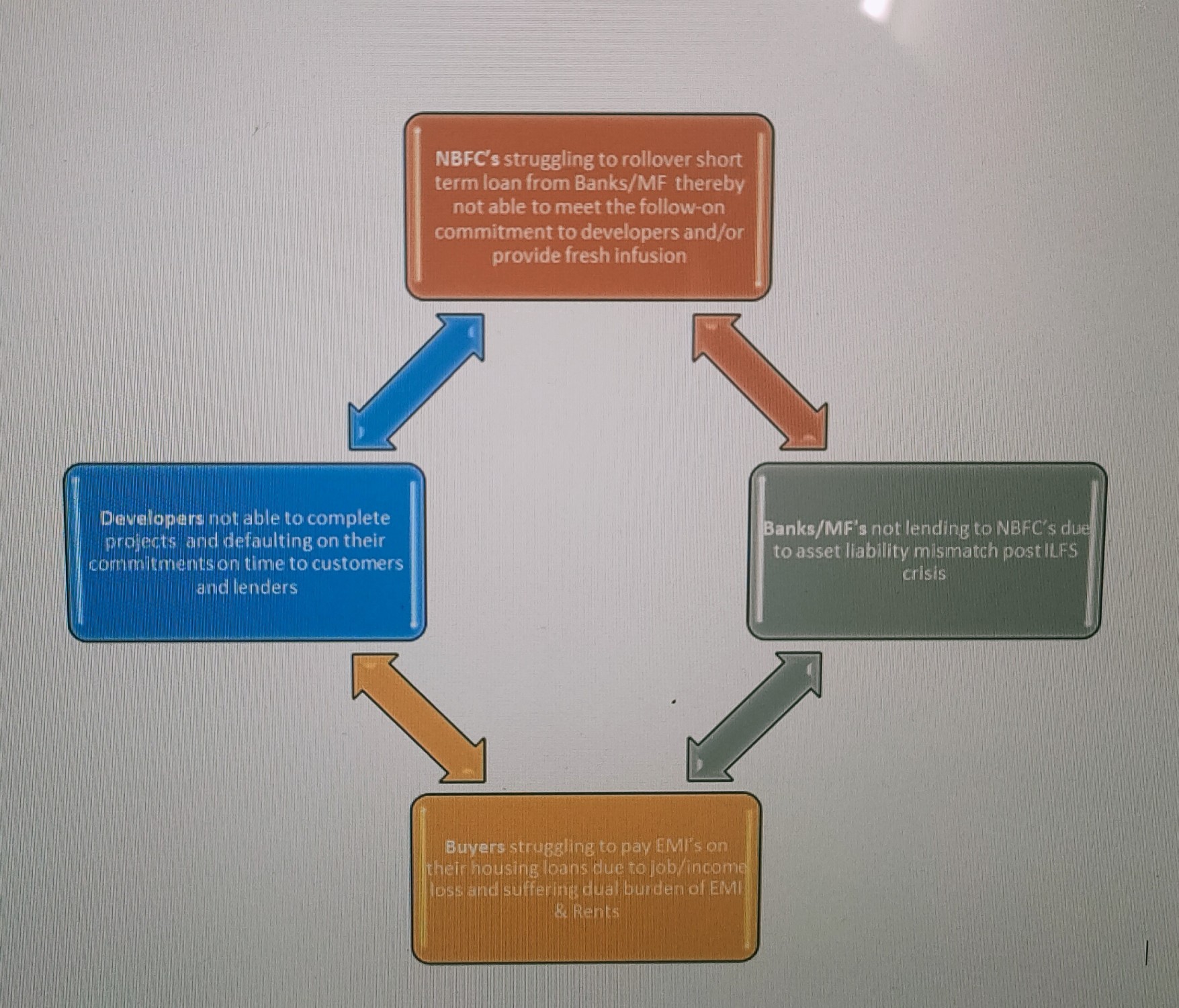

Since sales remained abysmal all this while, developers are finding it difficult to meet their debt obligation at this point. This resulted in significant project delays , sale price stagnation, debt pile up, companies facing insolvency putting all the stakeholders in jeopardy, with the unit buyer being worst hit. Hence resulting in a debt trap between the Buyers, Developer’s, NBFC’s and Banks.

The Debt Trap – ‘Chakravyuh’

Considering the Real Estate sector is the one of the largest employment generator, contributes significantly to GDP, significantly impacts the consumption spends of the stuck buyers, there is resultant loss of revenue on account of GST and stamp duty, mortgage lending forms large parts of FI’s balance sheet bringing stress and impacts more than 30 industries directly or indirectly, it is imperative to give a specific focus to the same and get it back on its feet. An AIF of INR 10,000 crs on first charge basis may not be enough to solve it. Some of the recommended actions may include,

- Existing standard loans to large under construction projectswith more than 50 units

- Should be brought under priority sector lending and existing facilities should be refinanced with follow on working capital funding made available to it from the banks

- Restructuring norms as recommended by K V Kamath committee for standard assets may not apply solely based on historical profitability and liquidity ratios, it should also consider residual net cash flow surplus of the project under consideration, the correct measure for a Real estate project

- Existing Non-Standard loan for under construction projects

- Firstly, One-time restructuring norms should be extended to the qualifying projects that are under construction & has residual surplus to complete the project and service the restructured debt & interest commitments

- Secondly, a similar line as SWAMIH fund, an AIF/ARC need to be established that can give exits or takeover the loans of the existing lenders/NBFC’s/Other AIF’s through One Time Settlement (OTS) where LTV is not enough to service the existing loans with applicable haircuts and provide secured patient capital to the projects/developers to complete the projects and have preferred return mechanism on the same. Banks can contribute to these funds under a Sovereign Guarantee umbrella and professionals fund managers with sector experience should be hired for each location for deployment under a central policy framework

- Non-Standard loans with developers undergoing Insolvency proceedings under IBC with NCLT

- None of the real estate project that had undergone Insolvency proceedings has got resolved due to its very unique nature as generally monies received from buyers for any project generally surpasses the amount contributed by any other financial creditors and thereby leaving the proceedings in the hand of the multiple buyers resulting in dead lock situation. The framework needs a clear authority of supreme decisive body that will take the final decision on the behalf of the buyers and that cannot be challenged by the individual buyers with limited vested interest. The authority may be constituted by the buyers through a referendum process and should involve people from IBC background, ex-Bankers and industry professionals.

This segment of stuck residential real estate buyers need a very specific attention at current times and focused resolutions can help clean the FI’s balance sheet , creates an multi-million employment revival opportunity and multi-billion distressed high IRR investment opportunity in the sector for Public, Investors and contributors only by solving the stuck projects over next 36 months

#realestateexperts #realestatedevelopers #realestateinvestors

#bankingandfinance

#nbfcs #housingfinance #realestatebuyers

Founder and Director – Pcube

linkedin.com/in/rajat-shail-kumar-b1951a10